A machine is bought for €15,000, it has a useful life of five years. At the end of the second year, its fair value amounts to €7,000, the cost to sell are € 2,000. Its cash flows for the periods 3, 4, and 5 are €3,000 each. Calculate with an interest rate of 10 percent.

The impairment at the end of the second year is equal to

- €1,539.44

- €7,466.56

- €3,000.00

Solution. A is correct.

First, we compute the recoverable amount.

recoverable amount = max{ future value is sold minus cost to sell; value in use}

= max{7,000 — 2,000 ; 3,000/1,1 + 3,000/1,1^2 + 3,000/1,1^3}

= max{5,000 ; 7,466.56}

= €7,466.56.

Therefore, an impairment of €1,539.44 needs to be added to the depreciation of €3,000 in the second year so that we have a book value of €7,466.56 at the end of the second year.

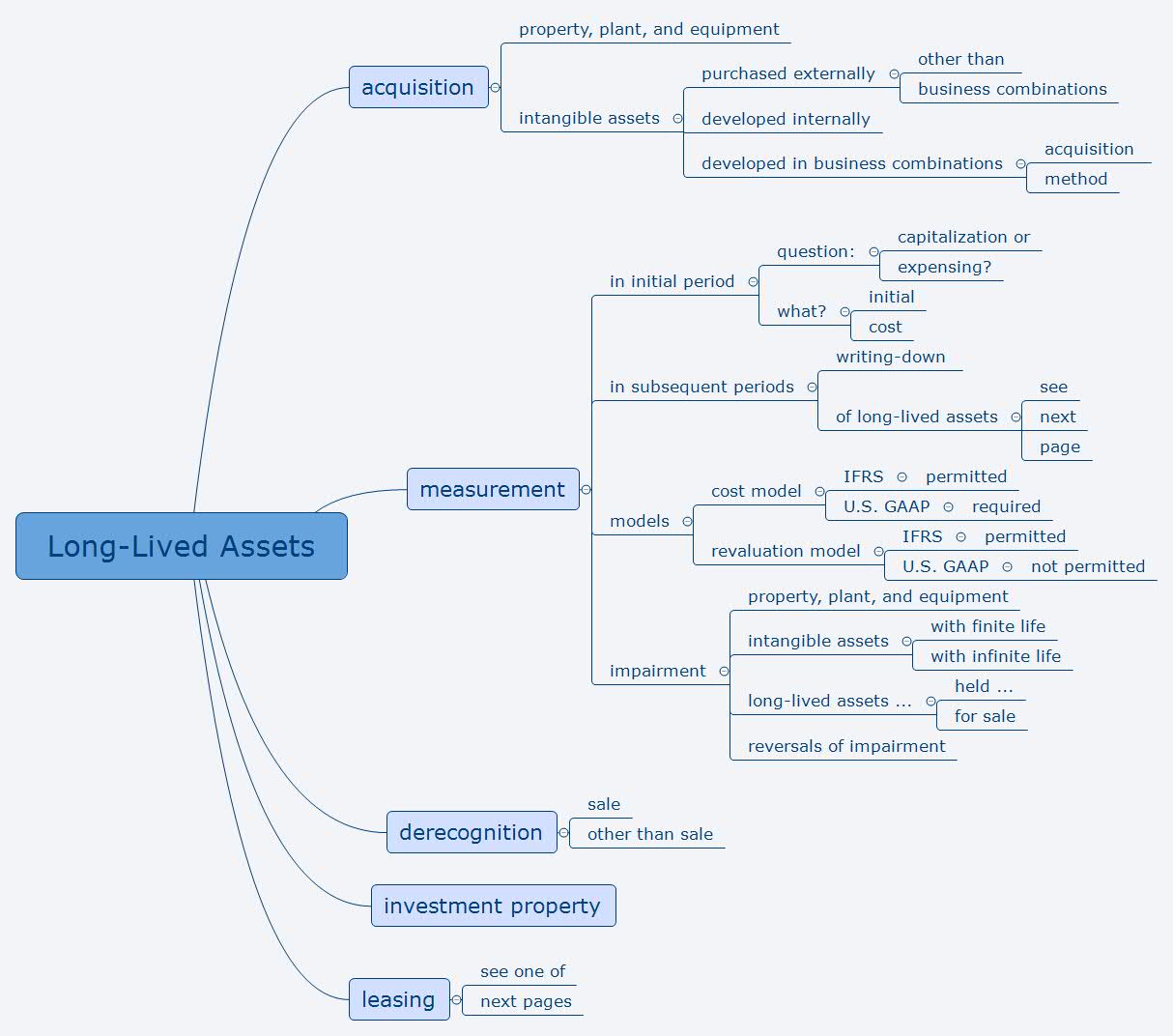

The most important points of Financial Reporting and Analysis, and Long-Lived Assets in this post can be summarised in this MindMap:

Did you find the MindMap helpful? All Lambert Education MindMaps for CFA Level 1 and Level 2 can be purchased in the online shop at https://daniel-lambert.de/produkt-kategorie/chartered-financial-analyst/

0 responses on "CFA Level I, Financial Reporting and Analysis, Long-Lived Assets, Impairment"