CFA Level I, Financial Reporting and Analysis, Long-Lived Assets

When talking about the balance sheet, we always need to consider:

- recognition,

- measurement,

- indicial measurement, and

- subsequent measurement.

In regard to recognition, we need to decide on whether or not to capitalize something, i.e. put it into the balance sheet, or not capitalize it, i.e. putting it into the income statement.

Measurement tells us with hoch much of something should be capitalized. Initial measurement is about cost, subsequent measurement needs to take into account the writing down of assets.

Writing down of an asset means that you are acknowledging that it is depreciating (in the case of tangible assets) or amortised (in the case of intangible assets). Depreciation or amortization will allocate the initial cost to the useful life of the asset. In the case of unforeseeable events that lead to a recoverable amount strictly inferior to the book value of an asset, we need to have an impairment.

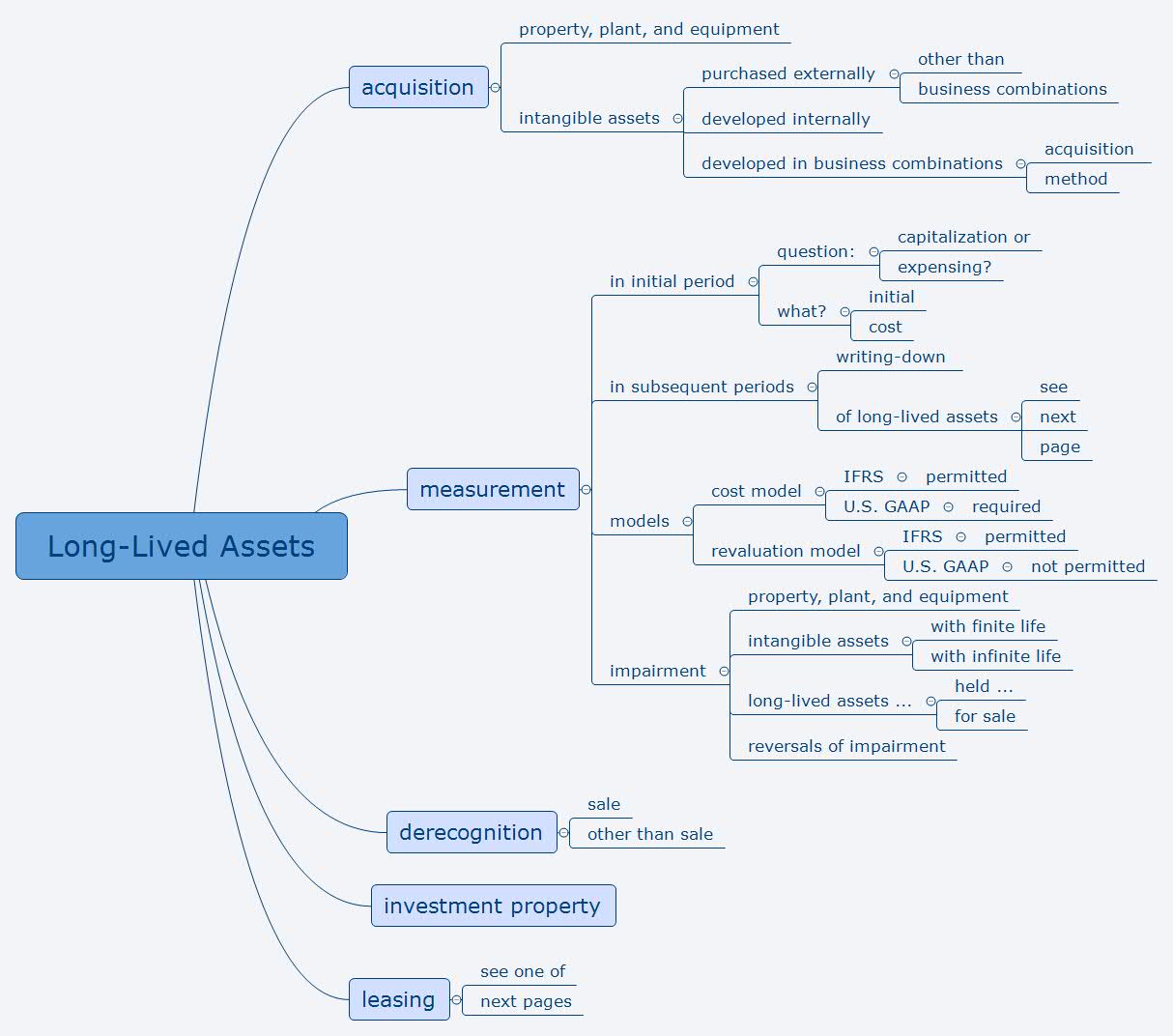

Find all important aspects of Financial Reporting and Analysis, Long-Lived Assets in the following MindMap:

All Lambert MindMaps for CFA Level 1 and Level 2 can be purchased on https://daniel-lambert.de/produkt-kategorie/chartered-financial-analyst/.

0 responses on "CFA Level I, Financial Reporting and Analysis, Long-Lived Assets, Recognition and Measurement"